According to market insights from Benchmark Minerals and prediction by McKinsey& Company we can see that the solid part of lithium is used for the EV batteries sector. On one hand it’s due to growing sales and adoption of EV worldwide, on the other hand a battery in an EV is simply bigger, then in other devices (smartphones, drones, electric boats or even golf carts).

That’s why the biggest names in the lithium ion batteries market are tightly connected to EV production, for example Tesla and BYD. Other ones are from consumer electronic giants: LG, Samsung SDI, Panasonic. But to many surprise the TOP1 position in this market is occupied by CATL – a giant and an actual lithium ion battery manufacturer and lithium ion battery supplier, for instance they cooperate with Tesla (especially for their EVs produced in China) and many other brands. CATL is known for LFP batteries (LiFePO4) – that are stable and safe compared to other chemical types of batteries.

This is not surprising that customers in the B2C sector are not familiar with wholesale brands, this is something we can observe in almost every area. Let’s just ask ourselves: who grows potatoes for McDonalds or produces milk for Dairy Queen? Of course, this is an abstract example, but we believe you understand what we mean.

Let’s have a look at who produces lithium ion batteries in-house for the world. SNE provided data about TOP10 EV lithium ion battery suppliers in 2024, and compared it with the same companies from 2023, we present it in Table 1. Please, have a look:

|

# |

EV Lithium ion battery suppliers |

|

Market share by year |

Consumption, GWh |

|

||

|

2023 |

2024 |

2023, Jan – Apr |

2024, Jan – Apr |

||||

|

1 |

CATL |

Ningde, China |

35.3% |

37.7% |

62.6 |

81.4 |

30.0% |

|

2 |

BYD |

Shenzhen, China |

15.8% |

15.4% |

28.1 |

33.2 |

18.3% |

|

3 |

LG |

Seoul, South Korea |

14.6% |

13.0% |

26.0 |

28 |

7.8% |

|

4 |

Samsung SDI |

Yongin-si, South Korea |

4.6% |

5.1% |

8.2 |

10.9 |

32.9% |

|

5 |

SK ON |

Jongno, South Korea |

5.9% |

4.8% |

10.5 |

10.3 |

-2.0% |

|

6 |

Panasonic |

Osaka, Japan |

8.1% |

4.7% |

14.4 |

10.2 |

-29.5% |

|

7 |

CALB |

Changzhou, China |

4.1% |

4.3% |

7.3 |

9.3 |

26.4% |

|

8 |

EVE |

Huizhou, China |

1.8% |

2.3% |

3.3 |

5.0 |

53.2% |

|

9 |

Gotion |

Fremont, USA |

2.3% |

2.2% |

4.1 |

4.8 |

15.8% |

|

10 |

Sunwoda |

Shenzhen, China |

1.6% |

2.0% |

2.8 |

4.4 |

57.7% |

|

Other |

5.8% |

8.7% |

10.2 |

18.7 |

83.0% |

||

|

Total |

100% |

100% |

177.6 |

216.2 |

100.0% |

||

Table 1. TOP 10 Lithium ion battery suppliers

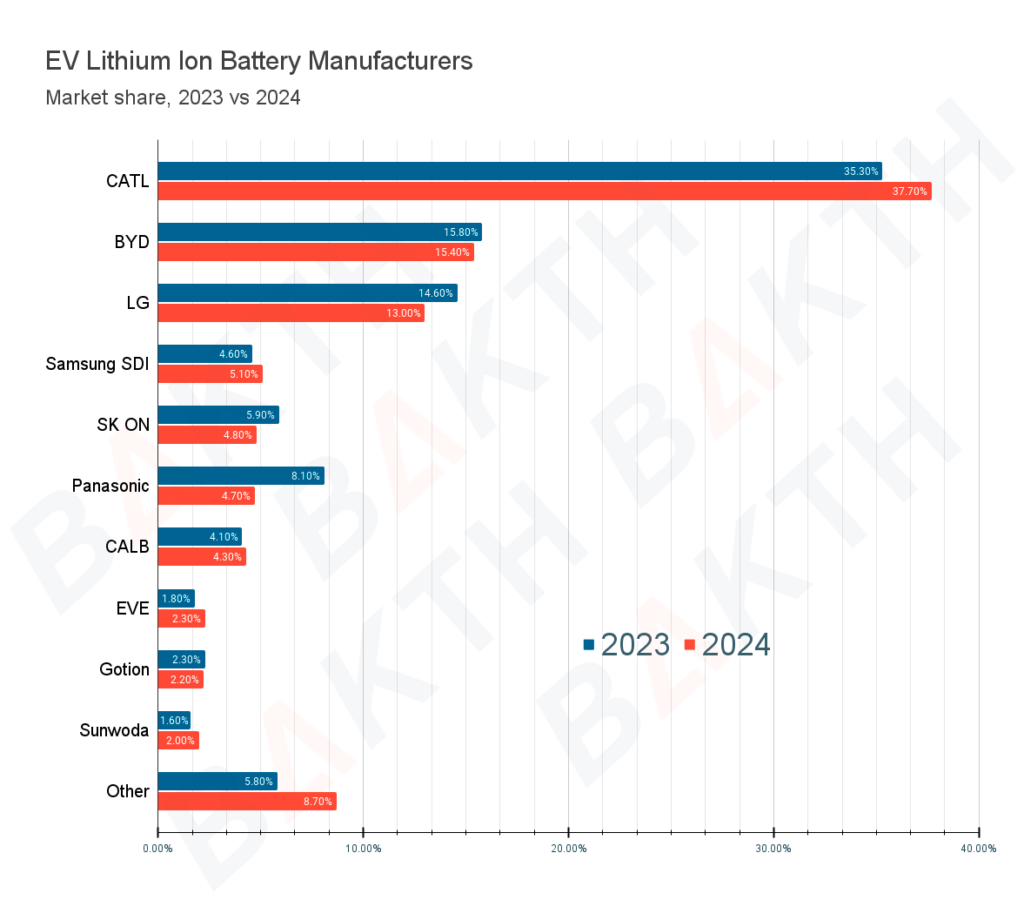

Let us get some insights from this data. Look at Chart 1. First of all we can see that CATL is the indisputable leader, and we believe it will stay in the front for quite a long time due to its efficient partnership with EV car manufacturers. BYD – is another great example of a success that was earned through car production. Generally speaking, for such enterprises it’s very important to keep production of batteries under control simply because of safety reasons. Yearly reports about supply chains allow us to verify that they indeed produce lithium ion batteries in-house.

A little marketing insight: the smaller the enterprise, producing its tech, is – the relatively less it worries about lithium battery suppliers. And vice versa. We have a feeling that this creates a positive reinforcing loop, where bigger corps tend to cooperate with greater suppliers, hence the biggest money stays within a smaller circle. It means, it’s harder for smaller suppliers to grow, unless their counterpart achieves significant success in the market and stays loyal to former partners.

We can see that market growth helped some companies change their presence in the market significantly, mostly those are smaller companies, that showed higher expansion rate: Sunwoda (57.7%), EVE (53.2%). Bigger companies showed more moderate growth: CATL (30%), BYD(18%), Samsung SDI (32.9%) etc. Some lost their power: SK ON, Panasonic. Especially interesting to see, that minor companies, grouped under the general label “Other”, expanded by 83% (from 10.2 GWh to 18.7Gwh), while the market itself only grew by 21%.

And the location of these TOP10 lithium ion battery companies is quite specific. Look at the Chart 2.

Let’s dive in and see in detail what happened to the leaders in past year.

Hard not to notice – the Chinese leader CATL, it dominates the market with a rise in share from 35.3% in 2023 to 37.7% in 2024. This growth highlights their strong position and efficient production scaling.

Second position in this list belongs to BYD, not surprising, this is also a Chinese lithium ion battery company. Its share is twice smaller then CATL, yet quite big: 15.4%. In past year we can observe a decrease from 15.8% to 15.4%. Bat that’s percentage, in general considering the market growth, BYD continues to show solid growth in consumption.

For companies outside China this year was more difficult. LG demonstrates a notable drop in market share: 14.6% in 2023 vs. 13% in 2024. Competitive pressures or shifts in supply chain strategies can be the result of what we see here. Having a decline while the market is growing – is not a good sign

For another South Korean lithium ion battery company, the year was better, Samsung SDI increased its market share from 4.6% to 5.1%. This success points to an effective expansion strategy with a 32.9% rise in consumption. Yes, we call it success! Keep it up, our dear competitors!

CATL saw a strong expansion rate of 30.0%, increasing battery consumption from 62.6 GWh to 81.4 GWh.

EVE from China leads with the highest expansion rate of 53.2%, reflecting aggressive growth and increased demand for its batteries.

Sunwoda, also from China, shows impressive growth with a 57.7% increase in consumption, indicating its rising market influence.

SK ON from South Korea and Panasonic from Japan both faced negative growth, with SK ON showing a slight decline of -2.0% and Panasonic experiencing a significant drop of -29.5%. These declines could suggest challenges in maintaining competitiveness or changes in client relationships.